EnergyPathways PLC - Investment Opportunity leveraging the impetus on Net-Zero, Right Place, Right Time!

Energy Pathways has started the year with real purpose, having landed NSTA Licence Operatorship approval for Block 110/4a that includes the Company's Marram Energy Storage Hub project (MESH). After a stellar 500%+ rise last year, can they surpass that in 2025?

Energy Pathways has started the year with real purpose, having landed NSTA (North Sea Transition Authority) Licence Operatorship approval for Block 110/4a that includes the Company's Marram Energy Storage Hub project (MESH) and signed a subsea engineering service agreement with PDi Ltd. After a stellar 500%+ rise last year, can they surpass that in 2025?

Company Overview

Listed on AIM in December 2023, EnergyPathways is a company looking to capitalise on the UK’s severe lack of energy storage and the government’s Net Zero focussed agenda by developing an integrated energy storage project that can provide the UK with a nationally independent, secure and flexible gas supply, whilst leveraging the growing value loss from the UK’s wind power excess by utilising green hydrogen production and storage solutions.

As a “first-mover” in a multi-billion pound growth sector, EPP has positioned itself as an attractive infrastructure investment with potential high-yield returns over a 20+ year project lifespan. With shareholder alignment demonstrated with circa 20% BOD “skin-in-the-game”, EPP could be a promising investment both short and long-term.

What is MESH?

No matter what your thoughts are surrounding the push for Net Zero, the MESH project actually appears to be a very good idea, both for domestic energy security and as an investment.

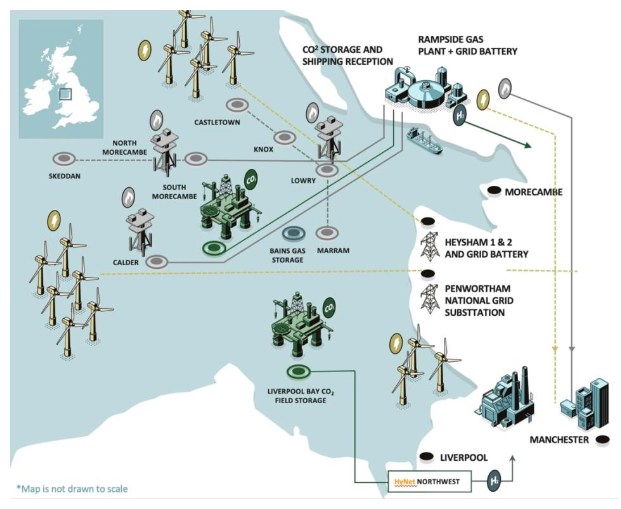

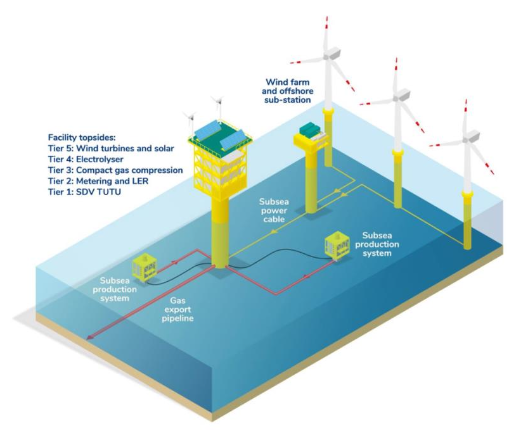

Situated 11 miles off the Lancashire Coast, EPP holds a 100% stake in the Marram Energy Storage Hub project (MESH) and is ideally located for energy storage with the highest population and industrial demand outside of London nearby and a comparative case study project in the HYNET Cluster adjacent. Also, as well as benefitting from high-quality geo- storage reservoirs, MESH is surrounded by an expansive 7-8GW of planned and existing offshore wind farms in the Irish Sea. The overall aim will be to provide the UK with a secure and reliable supply of natural gas and green hydrogen for over 25 years. Let’s take a closer look at what’s involved.

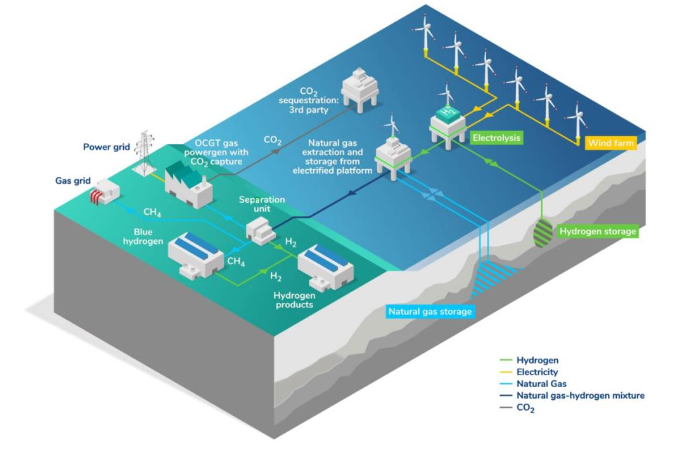

The MESH project is a rather elegant concept and, in its first phase, will produce natural gas from the Marram field (Fully appraised, 100% owned, with 46bcf gas), for which it has just been granted an Operatorship license. As the gas flows, the subsea caverns will be emptied, allowing the reservoirs to be utilised for gas storage. The aim will be to store natural gas in one zone and green hydrogen in another.

Where will the Hydrogen come from, I hear you ask? Well, what makes this project so interesting is that EPP will take excess energy from nearby wind farms and convert it into Green Hydrogen using electrolysis. It will then be stored and sold to offtake partners along with the natural gas. The production and storage of green hydrogen is a major string to their bow, diversifying revenue streams and ensuring less exposure to natural gas price fluctuations.

MESH is also designed to be a fully zero GHG emissions facility and will be electrified by the same nearby wind farms with clean, green energy and, being so close to existing late-life gas pipelines, gas processing facilities and offshore transmission lines, MESH can use these to readily connect new energy supply to the UK market via this existing infrastructure.

Overall MESH will have a gas storage capacity of circa 15 TWh (around 50bn cubic feet of gas) and will be an equivalent size to Centrica’s Rough facility, currently the UK’s largest gas storage plant. Once online, MESH will increase the UK’s gas storage capacity by approximately 50% and it will be able to store energy equal to heating 2.5 million UK homes through winter. As for Hydrogen storage, MESH will have a 1.5TWh capacity.

But it doesn’t end there. EPP has already applied for additional gas production and storage licenses for the Knox and Lowry gas fields, which, if successful, would triple the project capacity to around 45 TWh or 150bn cubic feet of gas, therefore making it the largest energy storage hub in the UK. The expansion would also increase Hydrogen storage three-fold to 4.5TWh.

The project is currently in Pre-FEED (Front End Engineering Design), with this stage concluding in January 2025.

Final Investment Decisions (FID) is scheduled for the end of 2025. In addition, EPP has announced it’s in advanced discussions with several “Tier One” companies with the aim of forming a partnership consortium to take the project through to fruition. One of these partnerships, with a “FTSE 250 Engineering firm”, has already been confirmed, with Wood Group being named as the project’s Lead Engineering Partner.

A Global Oil and Gas major and one of the largest developers of wind power has also been mentioned as potential partners.

Why is it Needed?

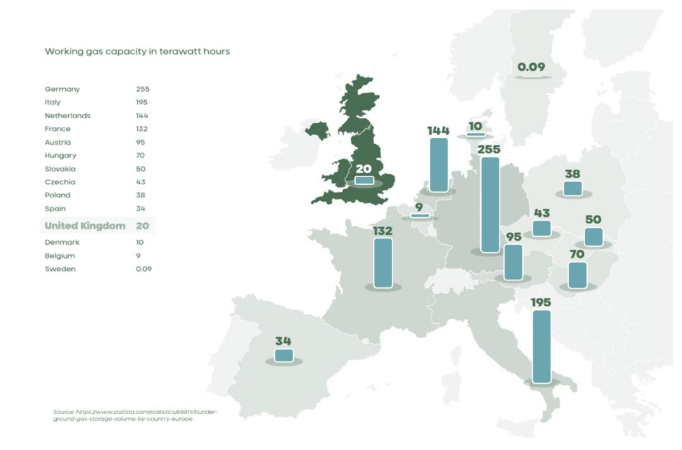

Currently, the UK’s working gas capacity is ranked 11th in Europe, behind the likes of Hungary and Slovakia and a mere tenth of the capacity of Germany and Italy.

As we have seen from recent geopolitical events, the need for energy independence is critical, and with recent headlines demonstrating the dire need for energy storage EnergyPathways appear to be in the right place at the right time.

The government are planning to invest billions into Net Zero projects, in particular Hydrogen storage, as part of their green agenda. But there is another key driver at the heart of this decision, and it comes down to pounds, pence and the government’s bottom line.

Every year, the government has to pay wind curtailment costs. This is because the government uses the Contracts for Difference (CfD) scheme to support wind energy projects. The CfD scheme guarantees a price for electricity generated by wind farms, wind farms like the ones surrounding the MESH project. Therefore, any wasted energy costs the government money. Currently, that’s a hit of £1bn a year and by 2030 it’s estimated to rise to £5bn a year.

How do they counter this drain on the coffers and the subsequent cost to the taxpayer?

The Net Zero 2030 policy is focussed on streamlining decisions regarding projects like MESH, ensuring they are fast-tracked and the hurdles to get to production/market are removed or reduced. It’s in the government’s best interest to promote the conversion of excess wind power to stored hydrogen. The stored energy can be used for a variety of applications, from heating homes to powering the Northwest fleet of hydrogen-fuelled public transport vehicles (another Labour-driven initiative).

The wind curtailment costs, as opposed to some green energy gimmick, is the reason why the government is striving to streamline the route to production for projects such as MESH and the neighbouring HYNET cluster and stimulate both public & private sector investment in the industry. Suddenly, the interest in Hydrogen storage starts to make sense, and given the amount of money MESH could save the government and, consequently, the taxpayer, it could well be in line for significant government grants and investment.

Comparable Projects and Financials

Down to brass tacks. The CAPEX required to get MESH through to full hydrogen and natural gas production and storage is projected to be £71m. This will enable the project to achieve a minimum gas storage capacity of 15TWh or 50bn cubic feet, which is the same size as the UK’s largest storage hub: Centrica’s Rough gas storage facility in the North Sea. Interestingly, Centrica has announced that to continue to function, it will need a CAPEX investment of £2bn (presumably all or in part from the government), a not unsubstantial investment by any standards.

As a comparison, MESH looks to be very good value for money, but should EPP also gain production and storage licenses for the additional Knox and Lowry assets, then the capacity of MESH as a whole would triple and dwarf that of Rough threefold.

So, say for instance, the tie-in of these additional fields added an extra £30m costs to the total CAPEX (I think it would be lower) and EPP could achieve Gas production/storage with a 45TWh or 150bn Cubic feet capacity and Hydrogen production/storage at 4.5TWh, all for a round £100m figure. What would be the more desirable investment for a public or private sector investor? Centrica’s 50bn cubic feet of storage for £2bn, or EnergyPathways’ 150bn cubic feet for £100m?

(In terms of research, aside from Rough, the adjacent HYNET cluster is worth looking at for a comparative business model in a latter phase stage.)

With regard to OPEX, EPP has raised £352,000 from converted warrants (equal to 3 months cash burn) and entered into a loan agreement with Global Green Asset Finance for a total of £5.1m. The loan facility is designed to support the MESH project through the FEED phase with a view to reaching FID at the end of 2025. Speculation as to whether the Loan provider CSM could raise the funds needed were set to rest last month when, as part of the agreement, EPP drew down the first £100,000. CSM has since raised over £700m in bonds and continues to bolster its position.

The Team

CEO Ben Clube brings to the table extensive experience and a direct, no-nonsense style to proceedings. Aside from a background in Geology, Clube was the Executive Director and Chief Operating and Commercial Officer of FAR Ltd, an Australian Gas explorer, from 2012 to 2018. During his leadership, he propelled the company to a AUD$655m market cap (£334m), gaining FAR Ltd notoriety as striking the “world’s biggest gas discovery” in 2014. Under Ben’s management FAR Ltd was widely regarded as one of the most successful Australian oil explorers for over a decade.

He also has 20 years' experience as a finance executive, including a role as Senior Vice President of Finance at BHP Petroleum. He’s served on the boards of UK and Australian- listed energy and resource companies, and more recently, he formed a start-up company to develop sustainable energy solutions with reduced carbon footprint. Ben has a track record of completing company-transforming commercial and M&A transactions creating significant shareholder value. In short, he brings extensive capital markets expertise.

It would appear the CEO has a vision and wants to deliver value to EPP shareholders, as well as himself, having considerable skin in the game holding around 6% of the company.

Some of what we can expect in terms of newsflow in the coming weeks and months:

-

- Marram Gas Storage License Decision

-

- Tier One Wind Power Partnership

-

- Tier One Oil and Gas Partnership

-

- Offtake Agreement: Gas Production

-

- Offtake Agreement: Gas Storage

-

- Offtake Agreement: Hydrogen

-

- Knox and Lowry Gas Production and Storage License Decision

-

- FEED Plan Completion

-

- Possible Debt Financing

-

- Government Project Shortlisting

Conclusion

I first noticed EPP a year ago and regrettably didn’t give it the time required to get under the skin of the project and its unique design. That oversight made me miss out on a 500%+ rise. The purpose of this article is to give a relatively bite-size, layman’s overview of what the company is all about, from the efficient business model to the advantageous political environment in the UK right now.

I see this as a key infrastructure investment with potential high-yield returns over a 20+ year lifespan of the project, a project that has been substantially derisked of late with EPP confirmed to be in discussions with the government’s DESNZ (Department of Energy Security and Net Zero) advisory committee regarding the hydrogen business model alongside major industry leaders.

Also, the announcement of Wood Group as Lead Engineering Partner, confirming Tier one talks have, in fact, been going on and successfully brought to sign off. Another green light was the drawdown of the Green Loan Fund and subsequent confirmation by CSM of the securing of £700m+ in bonds. This has quashed any doubts in terms of OPEX requirements through to FID.

Also, the granting of an Operator License for Marram is a ringing endorsement from the NSTA and bodes very well for the approval of the storage license and the Knox and Lowry applications. It would appear that, despite sounding very ambitious, CEO Ben Clube is managing to achieve what he says he will and in a more or less timely fashion.

The big issue for any new or existing investor is the £71m CAPEX needed to get the project off the ground. This, of course, is far too much to generate through a capital raise, so it would fall into two potential categories. First of which is that one of the large Tier One partners comes in with a debt financing solution, and the other generates the money through government investment and grants. In my opinion, it could be a combination of the two.

The Tier One names already RNS’d by the company as potential suitors will certainly have the capital to fund a project such as MESH. For instance, in the Irish Sea vicinity there is ORSTED a huge wind energy producer (and in my opinion the most suited partner for EPP). There is also BP operating in the area (another contender for the partnership consortium in my book).

Private sector aside, the government has allocated tens of billions for projects such as this and, from their perspective, an investment in MESH at £70-£100m is a fraction of the outlay compared to Centrica’s £2bn CAPEX requirement. It would also end up saving the government multiples of their initial investment through the avoidance of wind curtailment costs over the lifespan of the project. A no-brainer, it would seem?

Today EnergyPathways sits at a Market Cap of £14m, is on the cusp of FEED activities and has a wealth of news purported to be waiting in the wings. Also, rather interestingly, there’s only around 41% of the entire share issue in public hands as a free float, hence why the SP can achieve the blistering rises seen in the last half of 2024.

With many funds and institutions divesting from fossil fuels entirely or allocating dedicated funds for Net Zero and Green Energy projects, I am sure EnergyPathways will become an attractive prospect for institutional investment once certain market cap milestones are achieved and with a small free float, it could be an explosive cocktail.

In my opinion, it’s an investment that offers significant upside if certain factors fall into place, namely the tier one partnerships and debt financing, and there is, of course, always the chance of a buyout by a major before the FID later this year.

As we know, AIM and the small-cap arena is fuelled by sentiment as much as fundamentals (if not more) and projects like MESH garner a lot of media attention. The flames of which will inevitably be fanned by the government for the good of the government. MESH will help reindustrialise the North of England and stimulate employment and bring about the sort of feel-good success story the Labour government will champion at every turn. Let’s be honest, Ed Milliband isn’t shy of a HiVis Jacket photo opportunity and projects like this will be his legacy.

Whatever your thoughts about Net Zero, from an investment perspective, go where government money is being funnelled, and EnergyPathways seems to be very much in the right sector at the right time.

Image Credits: EnergyPathways PLC

Content Contributed by Thom Hudson