Goldstone Resources: At £8.5M Market Cap is this the Cheapest UK Listed Gold Producer ?

Goldstone continue to increase gold production at Homase with the latest gold pour a MoM increase of 10%. With the company expecting to hit a monthly 1000oz doré target this quarter, at the latest gold price, this equates to some $22M in annual revenue

With Gold on the cusp of breaking-out and looking like it's set to challenge this years ATH of c.$2800oz, Goldstone have continued the company turn-around with two consecutive MoM gold production increases, a product of stacking 48,000 tonnes of agglomerated ore per month which the company say will be maintained and allow them to achieve the target monthly gold doré production rate of 1000oz pcm.

As explained in previous articles, Goldstone initially suffered a number of technical issues that are now resolved, however the resulting depressed share-price doesn't yet reflect the remedial actions the company has successfully implemented, proven by increaased recoveries and continuos MoM increase in gold production.

Share-price decline reflecting early production issues. With issues sorted and gold prouction increasing entry-level could be atractive

The company now seem firmly on-track to deliver their 2025 objectives which at current gold prices and a production rate of 1000oz pcm return some c.$22M in annual revenue. This amount of revenue is not insiginificant for Goldstone currently Capped at just £8.5M!

The company also recently reported that they have agreed a debt to equity deal, regarding their Blue Gold CLN (£2.7M). Under the deal, Blue Gold's secured lender Davenport will receive equity in the company at 3.25p with some additional consideration shares, collectively amounting to c.16% of the companies issues share capital. Whilst this is dilutive, it's a step forwards and removes the debt from the balance sheet, allowing Goldstone to generate cash, focus on operations and its expansion strategy.

Expansion

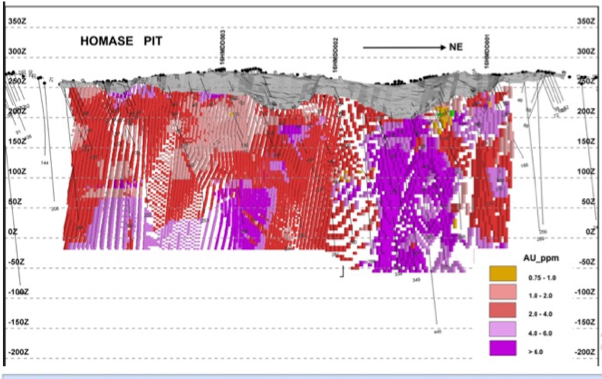

Whilst the company are now a producer and their sole focus has been on stabilising and increasing production at Homase, Homase itself offers some particularly attractive expansion upside, something that Goldstone have been planning to exploit. Why? well because the gold here grades at more than 6g/t and tapping into that would dramatically change the face of the company - it would require a different operating method, for mining and processing, but it would increase production and lower overall costs.

Purple areas show target gold with grades >6g/t

Purple areas show target gold with grades >6g/t

With the debt-position eased and the company increasing production, the FCF generated can be deployed into the expansion programme which should be further transformational for the company considering the grades of gold mentioned.

And we've not mentioned yet, Goldstone's 100% owned Akrokeri Mine close by where the board believe the historic head grade mined was an average of 24g/t.

At £8.5M Market Cap, and potential target annual revenues of c.$22M (@1000oz doré (68% recovery) pcm and Gold @ $2700oz) Goldstone could well be one of the cheapest junior 'Gold Plays' on the UK market if not the wider markets, in addition to offering significant growth-upside from within its current portfolio.