Graphite: It's time to look at Graphite Miners

Benchmark Minerals Intelligence report more than 300 new graphite mines will need to be built before 2035 to meet the demand for electric vehicle and energy storage - What options are there for UK Investors? Well not many!

Graphite remains the slightly more mysterious of minerals from an investors perspective, largely due to China's dominance in the market-place and the lack of pricing data. For example it's far easier to take a view on base metals such as the likes of Nickel and Copper where investors can access price information from exhanges such as the London and Shanghai Metals exchanges.

In contrast, accessing graphite pricing information is more difficult as graphite prices can vary depending on the quality, purity, and mesh size. Furthermore, there is little transparency around the individual pricing contracts executed in the market place. Factors that will affect the price however are supply and demand, quality and purity, mesh size and given China's dominance the value of the Chines yuan!

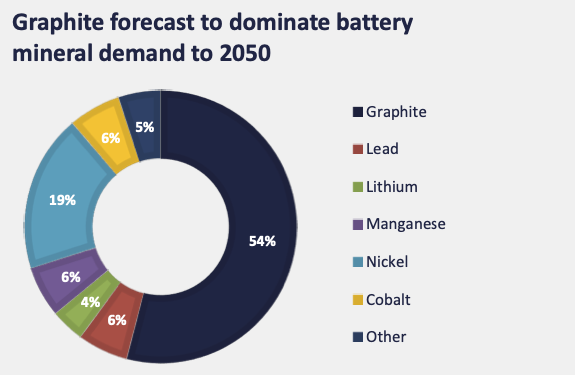

Graphite is however forecast to dominate battery mineral demand to 2050 and demand for batteries will compound 30% year-on-year to 2030 led by Li-ion batteries in electric vehicles. More than 300 new graphite mines will need to be built before 2035 to meet the demand for electric vehicle and energy storage batteries according to Benchmark Minerals Intelligence, so looking at viable companies/projects now looks like good timing.

Source Benchmark Mineral Intelligence

Source Benchmark Mineral Intelligence

Political Headwinds

With Trump back in power and the threat of tarrifs looming there are some considerations that could positively impact non-chinese suppliers of graphite, particularly suppliers of active anode material (AAM)

- China is the world’s largest producer of natural and synthetic graphite. If tariffs are imposed on graphite imports from China, U.S. buyers could face increased costs, potentially benefiting non-Chinese producers (such as African) or domestic suppliers.

- Tariffs could disrupt global supply chains, affecting industries relying on graphite for batteries, electric vehicles, and energy storage.

- Not only the US, but the EU are looking to reduce dependence on China as evidenced by the international 'SAFELOOP' consortium managed under the European Commission's €100 billion Horizon Europe Programme, focussed on the European Union's renewable energy transition. In fact 'Blencowe Resources' (LSE:BRES) announced recently it had joined the Elite European Commission Consortium to Exclusively Supply Graphite Concentrate for European EV Buses, article here.

- China itself, imposed export controls on certain graphite products back in 2023. The impact of these export controls was significant. In the first two months of 2024, China's graphite exports dropped sharply, with flake graphite exports decreasing by approximately 77.7% compared to the same period in 2023.

The export controls imposed by China have prompted global industries to seek alternative graphite sources to mitigate supply chain disruptions which is why the US and EU are increasingly supporting African-based natural flake graphite projects, the likes of Syrah and Blencowe two exmples!

Miners Though are Having to Adapt

Astute graphite mining companies are now realising that to attract funding and create realistic returns for both the company and shareholders, they need to be involved in the 'downstream' side of the industry, particularly where smaller flake graphite is concerned (the graphite used in EV batteries).

Larger and Jumbo flake sizes are less of a concern, as this product sells for a lot more than the few hundred dollars per tonne which small-flake concentrate sells for currently, into Asian markets. Companies need to ensure however that their 'basket-price' covering their overall product distribution is well in excess of the cost to produce!

Syrah Resources, one of the more established graphite companies has adopted this approach, becoming the first commercial-scale vertically integrated natural graphite 'AAM' supplier outside of China.

For junior graphite mining companies in particular, that may have high grade, high purity, good projects of scale, it may still not be enough to enter the market as a graphite concentrate supplier unless their production costs are in the lowest quartile. This is sadly why many junior graphite mining companies may never achieve funding and make it to production.

UK Listed Options - There aren't Many !

There are a few interesting graphite companies listed on the ASX including the likes of Syrah Resources and Renascor Resources which stand-out, obviously Syrah being one previously discussed and in production and Renascor who are post DFS stage with funding intent from the Australian Critical Minerals Facility. Un-surpsingly their Market Caps reflect the progress and stages they are at trading at A$270M and A$150M Market Caps respectively.

There is appetitie for Graphite funding but you will need to pick the 'cream of the crop' as, as previously discussed, many other listed graphite "want to be's" simply 'wont be' and achieve funding.

In terms of UK listed options, there aren't many, and as mentioned it will not be enough to say you have a high-grade graphite project, those companies will have to demonstrate through a robust DFS (Definitive Feasibility Study') that their projects are viable.

For example, Blencowe Resources (DFS due for completion around mid-year) will have spent c.$15M on their DFS in contrast to Armadale Capital (since de-listed) who spent under a 10th of that - a bit of drilling, a bit of testing and a desktop study is simply not enough!

Tirupati Graphite (TGR) MC - £9M an entrant to the London Market a couple of years back is a small-scale producer of graphite in Mozambique, the company is however suspended due to failure to complete an audit and further suspension of the companies co-CEO. This doesnt bode well for any investment case and is pretty much a non-starter until clarity comes!

GreenRoc Mining (GROC) MC - £4M are progressing the high-grade Amitsoq graphite project in Greenland. The project is at PEA stage and the company have made an application for an exploitation license. Whilst the project is promising, the company will face similar challenges to that of other junior mining companies in terms of raising capital to fund a DFS to the level required for funding. The company have reported a Funding LOI from the Export and Investment Fund of Denmark for funding directed towards the purchase of equipment as well as services from FLSmidth a/s and other Danish suppliers.

Sovereign Metals (SVML) MC - £220M

Sovereign Metals is a dual listed (AIM/ASX) and focused on its Kasiya Rutile-Graphite Project. Kasiya is the world’s largest natural rutile deposit containing both titanium and natural flake graphite. Despite the company being in the DFS stage, the market cap sits at a whopping $445M. Notably, Rio Tinto have invested in Sovereign to the tune of a 19% share-holding which will have helped endorse the project and send the market cap to its current-level. Perhaps notable here is that the right projects will attract partners/interest from majors.

Blencowe Resources (BRES) MC - £13M

Blencowe Resources are in the later stages of completing a DFS for their world-class Orom-Cross graphite project in Uganda. The project stands-out amongst peers for being an estimated 2-3 billion tonne, low cost, high margin project. As mentioned earlier in this article, from inception, Blencowe will have spent c.$15M (in excess of the companies current market cap!) on their DFS to ensure it is robust and meets financing requirements.

Notably Blencowe secured $5M of that funding via a US DFC (Development Finance Corporation) grant. The result of this is the company have controlled dilution well - a challenge mentioned earlier for juniors.

Perhaps what separates Blencowe apart from the pack, not withstanding it's tier1 graphite project, is its strategy, achievements and the partnerships it's developed to date including:

- US DFC Grant Funding and LOI for debt-financing of Orom-Cross

- First off-take MOU agreement for 15,000 tonnes of blended large flake graphite (66% of large flake product)

- Conversion of 600 tonne bulk sample to 96% concentrate confirming 'commercial scale' product

- SPG (Spheronized Purified Graphite) Large volume of battery-ready uncoated SPG produced from Bulk Sample

- Successful Micronisation testing completed at AETC in Chicago producing all five key product ranges.

- Successful certification of Environmental and Social Governance (“ESG”), policies and procedures

- MOU signed with two prominant SPG partners for Graphite Beneficiation facility in Uganda

- Global MSP Accreditation opening additional funding avenues

- Invitation to Join Elite European Commission Consortium to Exclusively Supply Graphite Concentrate for European EV Buses

Investors would be hard pushed to find another junior mining company that have struck-up so many Tier-1 partnerships (including funding) and particularly with two leading SPG specialists in China that will be paramount to successfully establishing an SPG facility in Uganda to produce AAM (a highly specialised technology)

For Blencowe and investors, there is likely a big value 'inflection point' over the coming months as the company complete their 6,500M drilling campaign (increasing resource and reserves), one of the final steps to completing the DFS which will show-case both the Orom-Cross Project and SPG Beneficiation Facility.

With funding options advancing (DFC and others), Blencowe have a realistic target of entering small-scale production by early 2026 (5000tpa concentrate) meaning the company will join the ranks of existing producers /miners within 12 months.

All the above for currently £13M Market Cap.

As mentioned earlier in the article, non-chinese graphite companies that can leverage the downstream AAM aspects of the market like Blencowe intend to, and sell their end product for up to 10x that of small-flake concentrate look to be clear winners, if they can prove to financiers that they have a robust project and the commercial-nouse to bring them to fruition.