Oxford BioDynamics: An incredible turn-around investment Opportunity at sub £10M Market Cap

Veteran, 'company turn-around' specialist Iain Ross recently joined Oxford BioDynamics as Chairman. His mandate, to take a leading 3D Genomics company with a commercial-ready portfolio into the mainstream market-place via industry deals and partnerships. "I've never in-herited a portfolio like this", Chairman, Iain Ross.

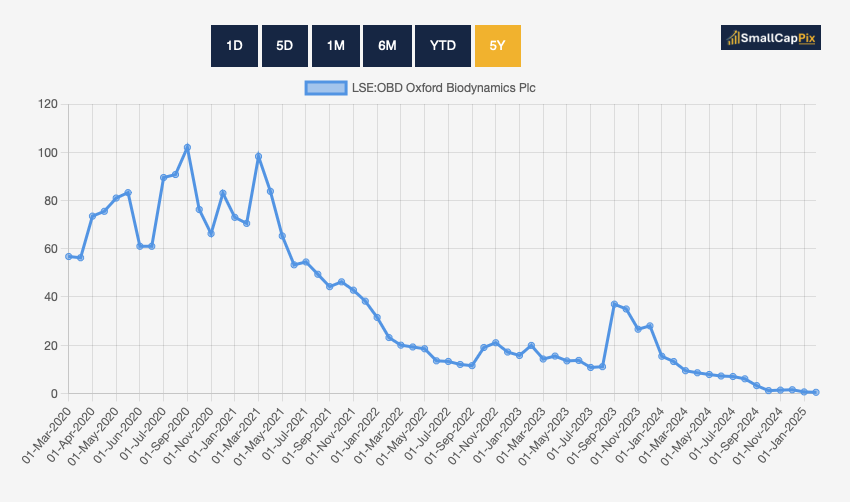

Every so often you stumble accross an investment opportunity that sounds too good to be true, they normally are, and if you looked at the Share Price chart for Oxford BioDynamics, you'd certainly not be licking your lips, however, having read up on the company and listened to new Chairman, Iain Ross, on a recent pre-fundraise investor call, I'm convinced that OBD could be one of the greatest turn-around plays that I'll expereience in my investing career 'if' new Management can execute, so lets dig into why I think this is the case.

Brief History

OBD was spun out from Oxford University in 2007 with the aim of translating fundamental scientific advances in 3D Genomics into a new generation of commercialized blood tests for life-changing diseases. OBD is making good on this aim, delivering both EpiSwitch CiRT, EpiSwitch PSE and EpiSwitch CST into the hands of doctors alongside a pipeline of other tests in development and about to hit the market.

It hasn't been plain sailing though. When the company IPO'd back in 2016 and in anticipation of brokering significant deals with Big Pharma, the company hit close to £3 a share, with a multi-hundred million pound valuation.

So what went wrong, and why the share price decline that sees the company valued at less than £10 Million today with c.£7.5M in cash? Well the simple answer to this from what I can gleen is, execution and poor business strategy where one can really only point the finger at management.

The reason I draw this conclusion and in fact, echoes the thoughts of new Chairman Iain, is that the company have successfully developed market leading tests for the likes of Prostate Cancer, Cancer immuotherapy/treatment suitability and others like COVID severe illness risk and Animal Health tests.

The portfolio is actually ground-breaking and the work OBD have done from a development perspective is nothing short of impressive. The problem is, and has been, the company are good at developing but not commercialisation. It's seemingly as simple as that, and investors would not wait around for deals and partnerships that didn't materialise, due to lack of focus and strategy.

That's about to change...

New Chairman, new Strategy

Iain Ross hosted a pre-fundraise investor call prior to the recent raise where he outlined why he has joined OBD and what he plans to do.

Iain has over 40 years' experience in the international life sciences and technology sectors having held significant roles in multi-national companies including Sandoz, Hoffman La Roche, and Celltech Group plc and is in fact very experienced in company turn-around and re-structuring including the likes of several biotech companies such as Ark Therapeutics, Redx Pharma, Silence Therapeutics and more recently, ReNeuron.

Along with the new Chairman, comes a new strategy and it's not rocket science, it's the simple realisation that OBD needs deals and partnerships to get their market-leading technology and products to market and this is something Iain has a wealth of experience in.

In fact Iain had been previously offered a role at OBD but couldn't join the company due to being in the middle of another company turn-around, however at the time, he said to the company, 'don't fall in love with the technology and try and take it to market yourself', they did, and hence whey the company were on the verge of administration until the recent fundraise.

Iain now has the cash runway (£7.9M raise) that should allow them to execute the deals and partnerships the company need. Iain also aims to bring in further non-dilutive funding over the course of the year to further extend that runway and 'turn the ship around'.

Over the course of the c.50 minute call I am in no doubt he has the capability to do this and if so, the company could go from zero to hero in a not very long time-frame given they have already developed the key products, some of which are being sold into the market already.

The Portfolio & IP

OBD position themselves as 3D Genomics experts and have developed their own EpiSwitch technology that translates into a number of key health tests the company are selling into the market. The company has laboratories in the UK, US and Malaysia.

Perhaps when you read through the following, you'll see that an EV of c.£3m for a portfolio of developed tests and the IP/Technology they are built on appears majorly undervalued. Well it is in my book!

EpiSwitch PSE

Perhaps the most prominant of OBD's current test offering is EpiSwitch PSE. 15/20 men currently having high PSA levels when doing a PSA test never go onto develop Prostate Cancer. However, a high PSA reading normally means an invasive follow-up biopsy of the prostate which is very uncomfortable and in worse cases can cause impotence.

This is where the PSE test comes in, using this in conjuction with PSA not only provides a 94% success rate in identifying prostate cancer/risk, it eliminates the need for follow-up biopsies saving time, money and pain! where on-going monitoring of the patient can suffice.

EpiSwitch CIRT (Checkpoint Inhibitor Response Test)

The worlds first test to assess the probability of therapeutic success of checkpoint inhibitor therapy with high accuracy. This test will help idenitify whether patients will respond to certain treatments and of course if not, the patient will not likely go through the process of a specific immunotherapy that is not only resource intensive, but a negative experience/outcome for the patient.

EpiSwitch Explorer Array Kit

The EpiSwitch® Explorer Array Kit facilitates unbiased 3D genomic biomarker discovery and profiling for academic and clinical R&D.

The above products and tests are already commercialised and generate sales for the company (i.e. the GoodBody Clinic use some of them and the company are in talks with the likes of BUPA which could be transformational), but going back to our earlier discussion, whilst sales are increasing MoM and there are promising discussions in progress, the company need to scale and the only way to do this in a short time-frame is partner up with distributors and other Pharma companies etc.

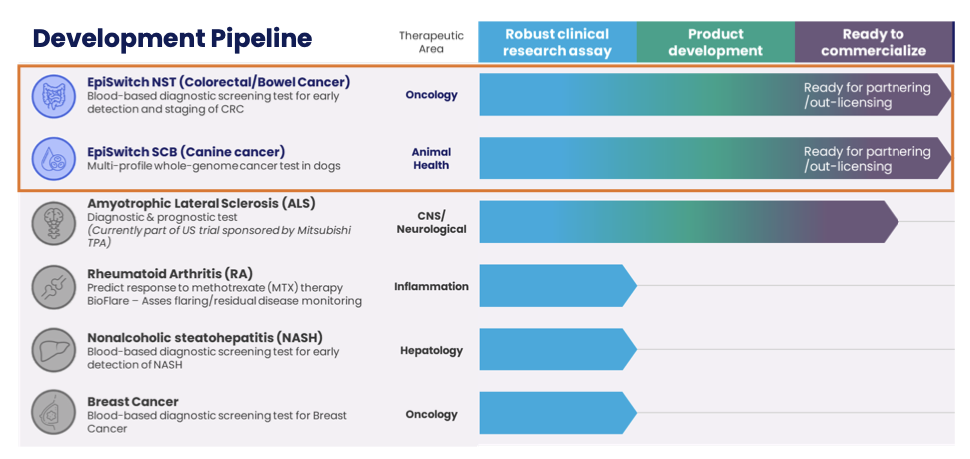

Pipeline

It's worth noting that the company are still doing what they are good at and have a pipeline of products/tests in development. The growing pipeline includes diagnostic/prognostic tests for early-stage detection and staging of prostate cancer and colorectal cancer, diagnostic, prognostic, predictive and monitoring tests in indications such as rheumatoid arthritis (RA), amyotrophic lateral sclerosis (ALS, also known as Lou Gehrig’s Disease or motor neuron disease), multiple sclerosis (MS), lymphoma and other cancers and, in veterinary medicine, a diagnostic/prognostic test for canine lymphoma.

EpiSwitch NST (Colorectal/Bowel Cancer)

This is another Blood Test for screening of Colorectal Bowel Cancer (early detections and removal of Polyps) and the product is ready for partnering/out-licensing. The NST Blood Test outperforms all other CRC tests and as such could be a major contributor to OBD's forward success.

EpiSwitch SCB (Canine Cancer)

This is a multi-profile whole-genome cancer test for dogs and again this test out-performs all other Canine Cancer tests. In a world where people treat their dogs a family, this test could make its way into the mainstream veterinary market-place with the right commercialisation and could again be a major milestone for OBD. This test is again, is ready for partnering/out-licensing.

Summary

You can see from the above that OBD are not an early-stage pharma company hoping to make a break, they've done it and have market-leading tests in most cases being the most accurate in the markets whether that be human or canine. Their technology alone is hugely valuable aside of sales opportunities, they have not yet capitalised on.

The likes of the FDA are also indicating that Big Pharma when developing medicines will need to accompany them with appropriate diagnostic testing, this is sensible, we shouldn't be treating patients with potential remedies when they arent going to work or add any value! This is where the likes of OBD will excel as they ramp-up their test portfolio or work on specific diagnostic tests as directed by Big Pharma. This in itself is a golden opportunity area of the company.

The Opportunity

So we have established a few things.

- OBD are without doubt experts in their field when it comes to development and facilitation of diagnostics

- The Portfolio they currently have with products in the market-place is market-leading

- The IP & Technology they have including EpiSwtich is a hugely valuable if monetised

- The Business is Scalable, they can develop endless amounts of new diagnostics

- The Company have failed to monetise their Portfolio

- The Company have not leveraged the correct partnerships or tapped into key markets

So we have a ready-made business, with an elite product offering that can be scaled and if so could see the company return to a multi-hundred million pound valuation (your penny per share today becoming pounds a share!) but it comes down to execution.

This is where Iain comes in. With his proven track-record in company turn-arounds his aim will not to be focused on immediate direct sales but on monetising the portfolio and quickly. This will take the form of strategic investment and pharma/distributor partnerships/royalty agreements, for example, working with the likes of LabCore and most likely where a partner will take a 'peice of the pie' but its much better to own 75% of a million pies than 100% of 1 pie!

So we are talking about the ability for the company to scale. An interesting point brought up on the call was that remarkably, OBD have had no conversation to date with the NHS which could use any number of these tests, future tests or even commission tests where the NHS could identify cost savings.

That is a massive failing on previous Management's part, however, Iain has already addressed this and put the wheels in motion. The company are also progressing discussions with BUPA and given OBD are a global company, have a number of other discussions in play.

So, the investment thesis here is straight forwards. You are betting on a company-turnaround and the Man to do it. You have hundreds of millions of pounds worth of potential value in the business trapped in a balloon just waiting to escape like the helium. That balloon just needs to pop and the value will start rushing out.

I hold a position in the company!