Blencowe Resources: The Path to Production

Blencowe Resources are entering a critical point in the valuation curve as they close out the last stages of the Orom-Cross DFS that will outline a 5 Phase approach to Blencowe becoming a major player in the critical minerals, graphite space.

Blencowe Resources are arriving at a value-inflection point having progressed their way through the project devlopment life-cycle culminating in an extensive DFS (Definitive Feasibility Study) that should be delivered in a few months time.

Blencowe will have spent some c.$15M to date on the project including the DFS which reflects the high-level of detail required to raise finance and secure offtake agreements, particularly in the graphite space.

A 'Desktop DFS' and limited product testing, simply doesn't 'cut the mustard'. If you are serious about becoming a producing mining company and raising finance, you have to invest in the DFS, this is what Blencowe have done with the following mapping out the journey to date:

The timeline and investment needed to become a successfull mining company

Along the way and in-line with Blencowe's strategy to differentiate themselves, Blencowe have built a number of key partnerships:

- US DFC - (Development Finance Corporation) $5M non-dilutive Grant Funding & Project Funding LOI

- MSP Accreditation - Mandate to bring crticial minerals supply chains to market - aditional funding sources

- Project SAFELOOP - Exclusive Graphite Concentrate supply agreement with the EU for EV Buses

- SPG Partnerships - MOU's with two SPG specialists that would see the development of an in-country SPG facility.

As we find ourselves today in a challenging market environment, when you consider the $15M project investment spend, the $5M grant-funding, the value of the actual graphite in the ground, lucrative partnerships and IP that comes with them and cash at hand, at c.£11M Market Cap, many would argue Blencowe has a negative Enterprise Value!

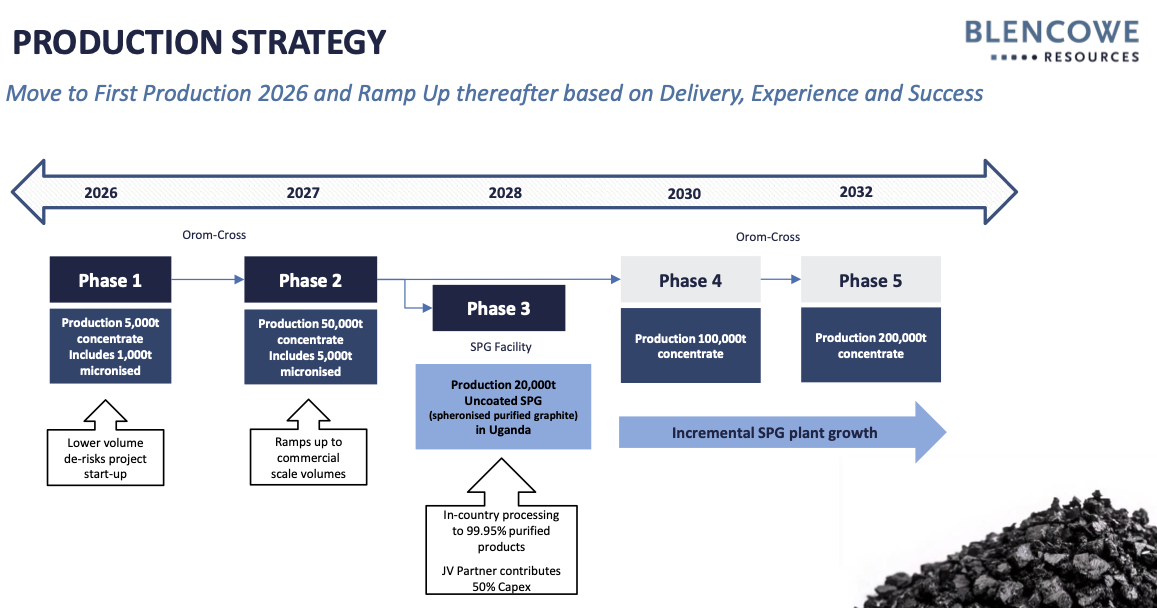

The Path to Production

The above infographic details Blencowe's plans for taking Orom-Cross into production and should give an indication of what investors can expect to see in the DFS.

The company have adopted a sensible strategy when it comes to production in that they intend to start from as early as 2026 with a smaller Phase 1 mining operation of 5,000 tpa concentrate increasing to a Phase 2 output of 50,000 tpa in 2027 and implementation of the SPG beneficiation facility in 2028 which would not only be a huge milestone, but would see Blencowe as only one of a few companies producing the 99.95% battery grade graphite product outside of China.

Post 2028, production would ramp up significantly and this expansion could be funded via organic-growth as the company will already be a major producer of graphite concentrate and SPG by this stage.

Funding

Of course, this plan isn't possible without the all important - funding.

The US DFC are expected to play a major part in this role, given their mandate to fund critical minerals projects, in the US interests, which has never been more important than now, with China's stranglehold on critical minerals and particularly graphite. In fact, Trump is already looking to shift foreign aid money into foreign investment facilitators like the DFC (which is his baby, created in his first presidential term) as outlined in a recent Bloomberg article here Trump advisers look to shift U.S. foreign aid to Wall Street ally

Syrah Resources in fact secured such investment recently Syrah Resources secures binding $150m loan agreement from the US DFC

But Blencowe are not limited to the DFC, their MSP Accreditation award opens further project funding avenues whereby South Korea, the current MSP Chair, proposed Orom-Cross for full accreditation at the MSP Members Forum meeting in New York in September 2024 where the proposal received unanimous approval.

In addition, there are yet further funding avenues such as the UK Export Finance body, UK approves use of export finance to secure critical minerals

Blencowe's funding strategy however, will probably incorporate a mix of debt and project-level finance. Investment at the project-level will be non-dilutive in equity terms and with the partnerships in place (i.e. the DFC), de-risking the overall project, project-level finance should be relatively easy to obtain off the back of a robust DFS.

Blencowe are currently completing the final 6,750m drill programme which includes some interesting targets and which will culminate in a JORC resource increase, being one of the final steps to complete the DFS. These results should feed through to the market soon followed by the DFS at which point, Blencowe will be in a position to close-out initial financing discussions and convert offtake MOU's to binding agreements.

Stay tuned as 2025 looks to be a pivotal year for the company and a signifiacnt value-inflection point for investors